Business and consumer confidence has risen strongly across the developed economies in the early months

of 2021 on the expectation that the worst of the pandemic is behind us. This is largely driven by the view that

a return to a more normal economic environment is much more likely as a result of mass vaccination. The international vaccine roll-out has been uneven to date, however, with the EU – including Ireland – lagging far behind the US and the UK, and the respective GDP projections reflect this disparity.

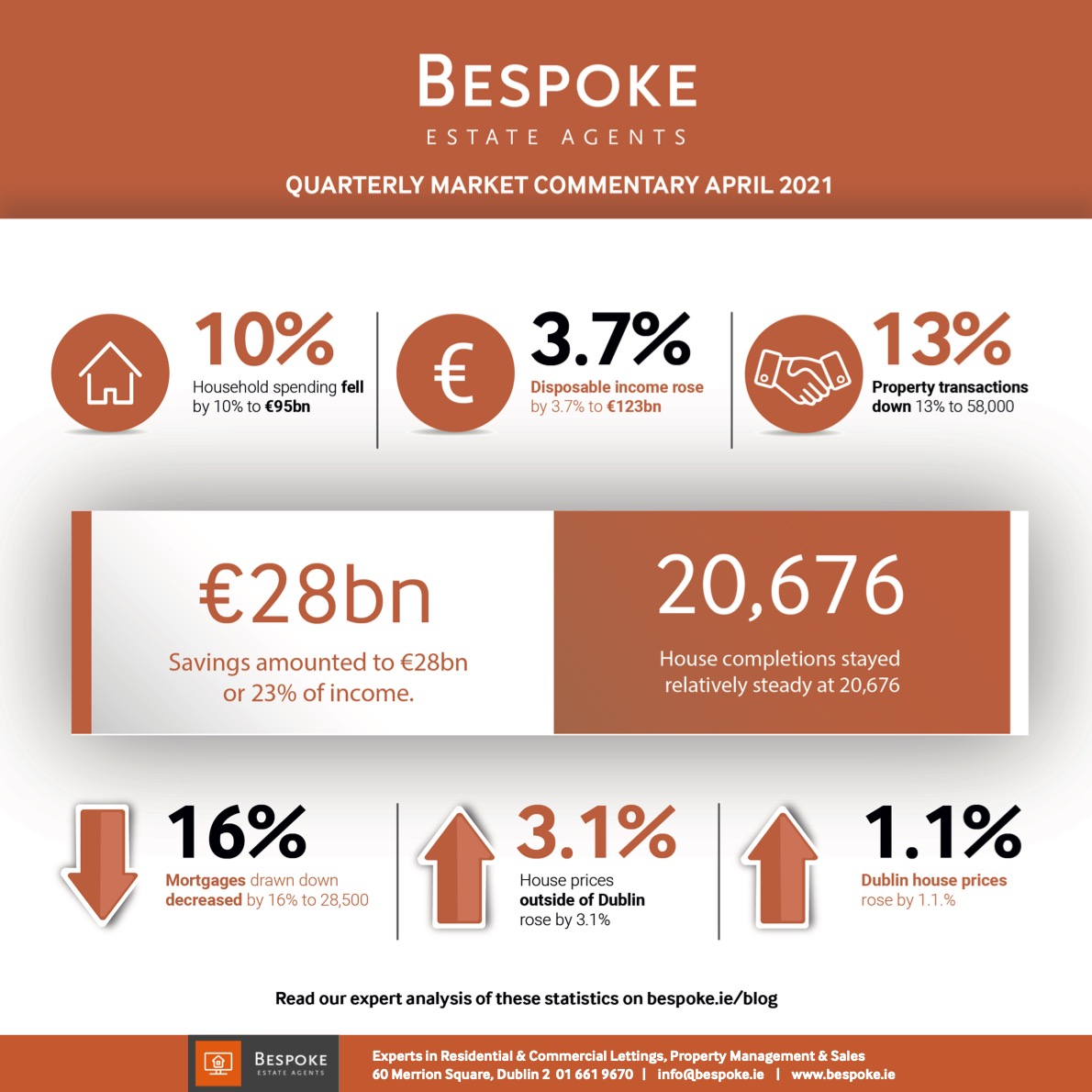

Residential property markets generally proved resilient despite the pandemic. Ireland had a similar experience in that prices excluding Dublin rose by 3.1%, with the capital recording a 1.1% rise, having recovered from negative territory earlier in the year. Transactions fell, nonetheless, by 13% to 58,000, while the number of mortgages drawn down for house purchase also declined, to 28,500 from over 34,000 in 2019, the latter a decade high. House building was severely impacted by the first lockdown and completions were expected to fall under 18,000, but in the event a surge late in the year resulted in a total of 20,676, only modestly below the 2019 build.

Rising house prices seem at odds with a headline figure of 600,000 unemployed but employment last year

fell by just 28,000 or 1.2%. The ‘unemployment’ total includes recipients of the Pandemic Unemployment Payment, who are technically still in work. Moreover, household income rose, supported by government transfers and wage increases in those sectors unaffected by the lockdowns, which are also industries where earnings are relatively high. This also explains why residential rents held up reasonably well if one excludes the Docklands area, where the ‘work from home’-related exodus of staff from the multinationals led to an increase in localised rental supply. This perhaps also explains the discrepancy in official figures on private sector rents in 2020, as surveys differ in terms of sample size and location mix; the CSO reported a 3.1% annual fall in rents in the final quarter of the year while the Residential Tenancies Board noted a 2.7% rise.

The generally negative tone from analysts on prospects for the housing market last year proved unduly pessimistic and the mood is more upbeat of late. This is in part due to optimism on the vaccine roll-out but it’s also related to a number of specific developments, with positive implications for house prices in particular. One is the probable impact of the most recent lockdown on supply, which on the face of it could reduce completions by at least 25%. Absent the shutdown in construction, completions may have reached 25,000, so it would not be surprising if the annual total for 2021 was well below 20,000.

On the demand side the Help to Buy scheme has been extended. First-time buyers can now reclaim up to €30,000 (it was €20,000) from previously paid income tax to fund a housing deposit, boosting their buying power. In addition, the lockdowns resulted in a massive increase in what was effectively forced savings by Irish households; disposable income rose by 3.7% last year, to €123bn, but household spending fell by some 10% to €95bn, so savings amounted to a massive €28bn or 23% of income. To put this into perspective, this is double the savings ratio seen in recent years. A large proportion of this excess saving has simply remained unspent in household accounts in the banking system, with deposits rising by €16bn over the past twelve months.

The Central Bank’s loan-to-income caps will keep a lid on price increases, despite the shortage of supply. However, absent a significant rise in unemployment in those sectors of the labour market that can afford to buy, it’s hard to construct a case for falling capital values. Total unemployment may well rise nonetheless, as some of those currently furloughed lose their jobs. Rents may also resume their rise as multinational staff return from abroad.

Of course, all this assumes that the vaccine roll-out continues to progress and the Covid-19 case load falls – it remains to be seen if further lockdowns are in store, but for now, consumers are optimistic.